I am not scintillated by the details of tax policy, so when I first heard the term owner compensation replacement, I paused just to think about what that might mean.

In general I am unlikely to engage in a lengthy debate about the nuances of tax rates, or shelters for certain funds, and despite some effort on my part I still can’t fully explain how an NFT works or even what it IS, except I will engage with the word “fungible.” I’m far more interested in helping people learn from my mistakes.

However, when the first round of PPP loans came, I was curious what might be in store for me. After all, I was a very new business owner having started writing for a living in 2018. So in 2020 when everything shut down and large companies were getting bailed out, I poked around to see what might be in there for a sole proprietor.

There was nothing.

The Payroll Protection Program was designed to do one important thing: help companies maintain payroll for their employees even during a time when they had to be shut down because of the pandemic. It provided up to three months’ worth of “payroll protection.”

The math was simple. I didn’t have employees, I didn’t qualify.

The third round of stimulus was different

As the pandemic wore on and the economy slowed to a crawl, the Trump administration gathered support for a second round of stimulus with the same rules as the first.

As the pandemic worsened, an election brought new leadership promising an additional round of stimulus. And the details were eye-catching. There was a promise for support for LLCs and sole proprietorships. Finally, a recognition that people who supported themselves were also struggling in many cases, and that they could use the same hand up.

We are, after all, a land of inventors, doers, sole proprietors … and we were in a major recession.

This third round of support included the Owner Compensation Replacement clause, offering needed help to sole proprietors and independent contractors who were paid solely through 1099s.

What is ‘Owner Compensation’ in the Payroll Protection Program?

To understand owner compensation, it helps to think of yourself as the employee AND the owner. You’re essentially applying for a PPP loan for yourself, only you’re not reporting any employees.

It is an acknowledgement that you ARE your employee, and lost income IS lost salary. The law allows for you to apply for up to two and a half months’ income.

And just like the PPP loan, you don’t have to prove that you lost that income, you just simply have to prove you were in existence prior to 2020.

And even better than the PPP loan, you don’t have to provide any evidence about how you spent it.

Owner compensation is just that: compensation. The new rules for this tranche of spending shows that legislators understand what it means to grow your own company, and that what you make running that company is your salary, even if you can’t yet afford to put yourself on the payroll. And even if you don’t have a payroll.

I run my own LLC, how can I apply for Owner Compensation?

Applying for Owner Compensation is so easy, even I could do it.

First, fill out your schedule C for 2020. Or, if you haven’t done that yet, you can use your 2019 schedule C. Don’t have it? You can find the form and the step-by-step instructions here.

(Also – beware the many places trying to sell you documents that you can get online from the government for free!)

Then, contact your bank. As with the PP loan, they are the ones who will facilitate the loan. They will provide you a link to the form.

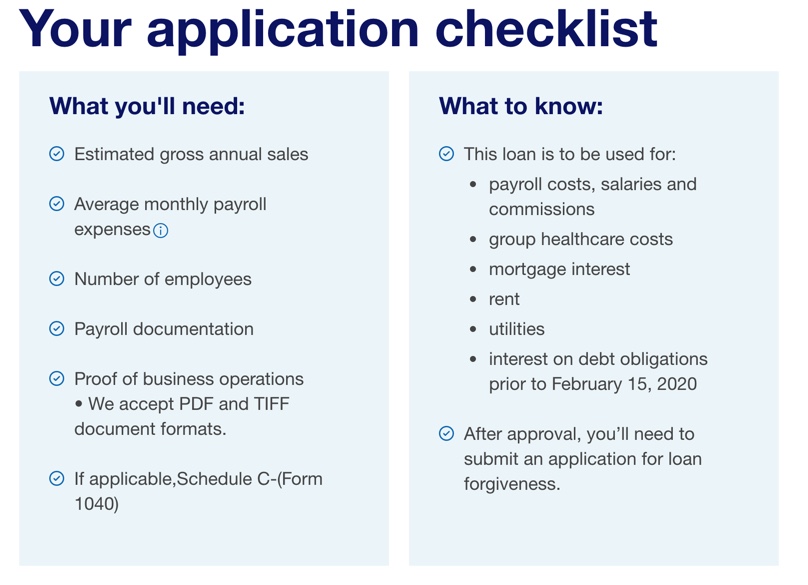

Next, fill out the Owner Compensation form. It is very simple and your bank’s site will guide you through the questions. The US Bank form started with a simple request:

Then a little more refinement …

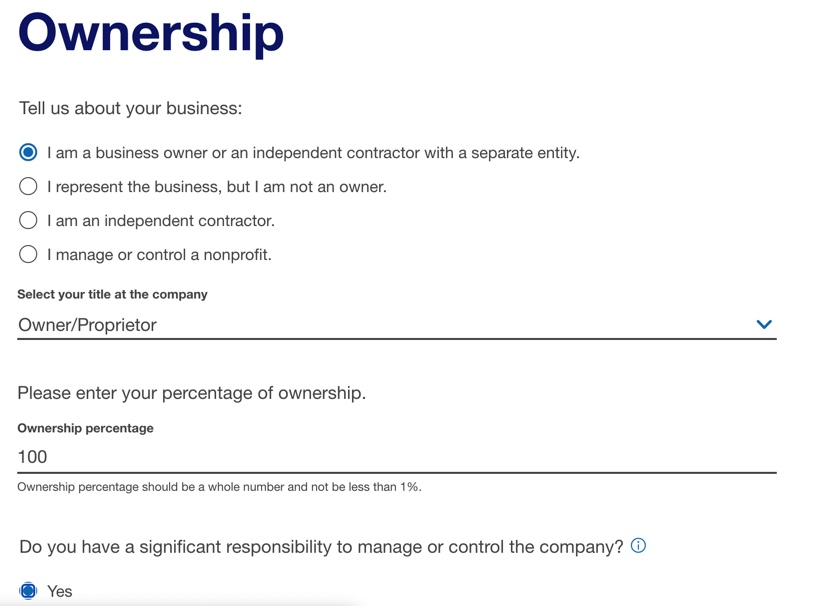

And a request for specific details about your business. (I needed to check my incorporation date with the state of Ohio, it was on my incorporation paperwork.)

Next, US Bank offered some assistance on which forms and information I would need to complete the application.

For me, the hardest part of the process was finding out the exact US government work code that describes my business – freelance writing and editing.

Now enter the amount of your loan request. You can apply for up to two and a half months’ compensation. You don’t get to choose your best two months, however. Instead, you must calculate by taking your year’s income, and dividing it by 12, and multiplying that by 2.5.

Here’s a video from Bench.com explaining how to calculate your Owner Compensation Replacement loan amount: https://bench.co/blog/operations/owner-compensation-replacement/

Then, hit submit, and wait.

It worked for one friend of mine, who shared this in an email:

I love it when I can help a friend out!

What about the PPP deadlines?

Different sites have posted different deadlines for filing. For instance, the Bench.com video (above) cites a March 31 deadline. The US Bank site says that applications aren’t being taken until May.

In reality, President Biden extended the deadline to May 31st.

It can be confusing. Don’t quit here.

Even if you are reading this article after that date, I recommend you finish the process anyway.

Why? There has been an abundance of goodwill. In fact, during the first and second waves of PPP loans, moving deadlines and general confusion meant that the money was being distributed until it was all gone. After all, money that doesn’t enter the economy doesn’t do anyone any good.

So just apply.

Don’t pierce the veil!

A word of caution to sole proprietors. Be careful how you ask people to pay you. When they pay you directly, by making a check out in your name, it is not the same as paying the business.

Remember, part of your reason for setting up a business was to establish it as a separate entity. This thin “veil” of calling your business something else protects you in the case that things go wrong.

When you accept and deposit a check made out to you instead of to your business, and you deposit it in your business account, you “pierce the veil,” meaning you sacrifice the protections that an LLC was providing.

Check with your tax preparer about how best to report this income on your schedule C, and whether it is wise to seek owner compensation by including this money.

What will you do with 2.5 months of owner compensation replacement?

I hope this helps you get compensation for the tough year that was 2020. Now, what do you plan to do with the money you get back? A website overhaul? Hire a social media manager? Hire a blog writer?

Let me know in the comments.

This article was also published on Medium.